Resources

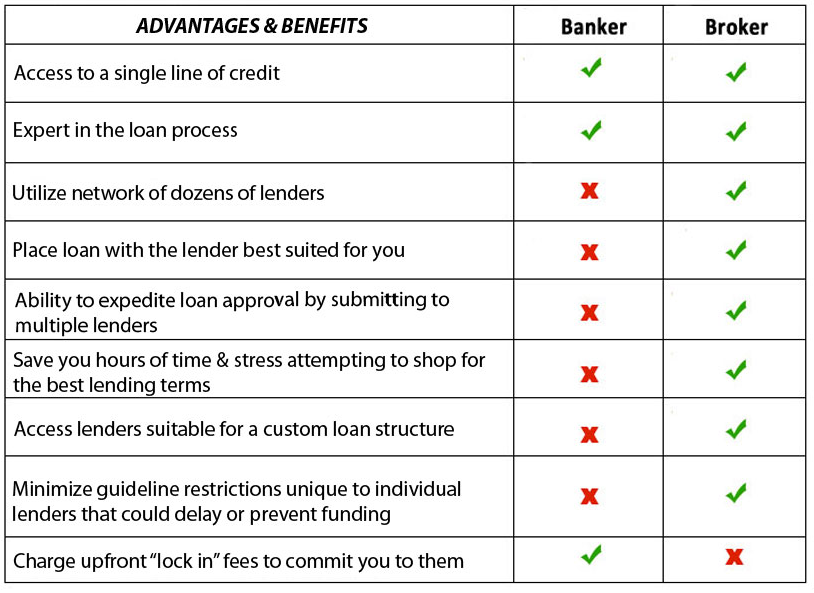

Why A Mortgage Broker Over Banker?

Closing Cost Explained

Non-Recurring Closing Costs (N.R.C.C.’s) – are fees which only occur one time and are directly related to the mortgage transaction (i.e., escrow fee, lender title insurance policy, recording fees, document preparation, notary fees, loan origination fees & or loan discount fees, appraisal fee and lender underwriting fees). Basically anything associated with the refinance and that occurs only once.

Recurring Closing Costs – (recurring expenses) are items, which will occur more than once on a regular basis regardless of whether you refinance or not (i.e., property taxes, interest and home owners insurance). In fact these EXPENSES and are not ‘hard’ cost directly related with the mortgage transaction

Prepaid Items – are items that occur and are to be ‘prepaid’ at the close of escrow for future obligations such as, 1st or 2nd half property tax installments , establishment of impound reserve account, yearly insurance premium dues to be paid in full, etc., (these can be paid either through the loan amount or by bringing in funds to close, however you choose.)

Non-Recurring Closing Cost – (illustration only)

- Appraisal fee

- Discount points (to buy-down interest rate lower – 2.00% max)

- Origination fee (points) IF any

- Credit report

- Processing fees

- Lender’s appraisal fee (usually paid up front)

- Document preparation

- Tax service

- Underwriting fee (lenders)

- Flood certification

- Wire fee

- Escrow fee

- Recording fees (county)

- Endorsement fees

- Loan tie-in fee (purchase loan)

- Notary fee

Recurring Closing Cost – (illustration only)

- Payoff interest on your current loan(s)

- Prepaid interest on your new loan

- Real estate property tax 1st or 2nd half installment due

- Homeowners insurance premium

- Mortgage insurance (IF applicable)

- Homeowner’s association dues – H.O.A. (IF applicable)